Why are the homebuilders so happy? | SkipLeadPro

Housing demand collapsed in 2022, and the homebuilders’ confidence survey looked like a waterfall collapse similar to during COVID-19 and the great financial crisis. However, something changed toward the end of 2022, and the homebuilders are now singing Party Rock Anthem as their confidence levels have increased along with their stock prices.

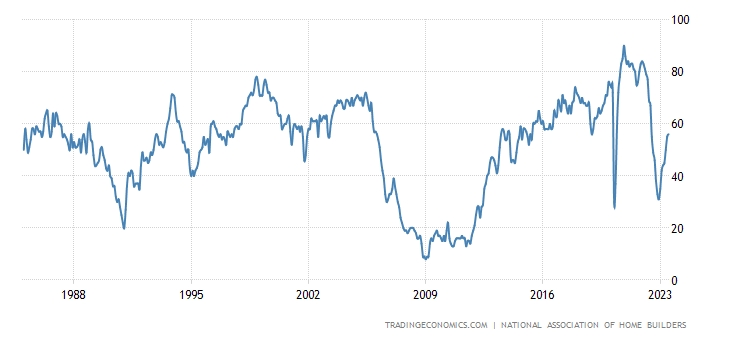

As we can see in the chart below, the NAHB/Wells Fargo Housing Market Index (HMI) data, which surveys homebuilders, is above 50 again. This means homebuilders are feeling confident enough to issue more housing permits, as we have seen growth in single-family permits the last few months.

The housing market, in general, turned on Nov. 9, 2022. (I go over that more in detail on this episode of the HousingWire Daily podcast.) However, even though the housing dynamics changed, existing home sales aren’t enjoying the growth in sales like the new home sales sector.

On Wednesday we got the housing starts data, and the builders are starting to push growth in single-family permits. Last year, people were talking about a second housing bubble crash, saying the builders had too many backlog orders to issue new permits. What a difference a year makes!

From Census: Building Permits: Privately‐owned housing units authorized by building permits in June were at a seasonally adjusted annual rate of 1,440,000. This is 3.7 percent below the revised May rate of 1,496,000 and 15.3 percent below the June 2022 rate of 1,701,000. Single‐family authorizations in June were at a rate of 922,000; this is 2.2 percent above the revised May figure of 902,000. Authorizations of units in buildings with five units or more were at a rate of 467,000 in June.

The builders are making money, not building homes to address the housing inventory shortage. They’re selling homes at the highest profit possible, which makes sense — it’s their business. Last year, we had the biggest one-year collapse in housing sales, but it didn’t create much active listing growth. Even today, we are near multi-decade lows.

From NAR data:

- 2007 total active listings: 4 million

- 2023 total active listings: 1.08 million, down year over year too.

Our demographics for home buying are better in the years 2020-2024 than in the previous decade; sadly we didn’t have enough product for them.

So the builders went to work making deals — they’re very efficient sellers. When they need to, they will cut prices and provide lower mortgage rates than what existing homebuyers are getting to move their product. They have done that as new home sales are up 20% year over year, while existing home sales are down 20% year over.

How? Their profit margins are still above pre-pandemic levels, so they have margin to spare, and not every home they sell gets this treatment either. Now you can see why their stocks have done so well. For example, I always reference Toll Brothers‘ stock price since the significant Nov. 9 date.

In this environment, homebuilders have an advantage they didn’t have before, as total active listings were too high, giving people more choices from 2007-2019. Now the builders have pushed down the monthly supply to 6.7 months, almost back to pre-COVID-19 levels, as the chart below shows.

This is why the homebuilders have been so happy lately and why their stocks have done so well. You can add this to the list of things that don’t happen during a housing bubble crash. Last year was a crazy year, and I understand why the usual housing bubble crash people went all in; I mean, it’s year 12 of the housing bubble 2.0 crash!

However, some other people who don’t usually fall for the crash premise joined the party, and as I have stressed for many years, using 2008 housing economic models simply doesn’t work this time. (See my debate last year with a stock trader on this subject here.)

Part of the problem I have seen over the last decade is that everyone is too focused on existing home prices crashing and not the economics of housing. Remember, economics done right should be boring and you always want to be the detective, not the troll.